Guide to Buying or Building a Home in Queensland

Deciding whether to buy an existing house or build a new one is one of the biggest financial choices most Queenslanders will ever make. This decision affects not just the cost of acquiring a home, but also the amount of time, effort and risk involved, the level of customisation available and the long‑term running costs of the home. Queensland, with its diverse geography, growing population and unique lifestyle, offers plenty of options—from charming character homes in established suburbs to brand‑new estates on the metropolitan fringe and bespoke builds on acreage. Understanding the market, incentives, regulations and processes that underpin the housing sector is essential for making an informed decision.

This guide aims to be a comprehensive guide for prospective home owners in Queensland. It examines the current state of the housing market, outlines the pros and cons of buying and building, explains government incentives such as first‑home grants and stamp duty concessions, demystifies the design and construction process, discusses sustainability and energy efficiency requirements, and offers strategies for managing risks and costs.

Queensland Housing Market Overview

Population and demand

Queensland’s population has grown strongly over the past two decades as interstate migration, overseas migration and higher birth rates increased the number of households. The south‑east corner—particularly Brisbane, the Sunshine Coast and the Gold Coast—has experienced robust growth as people seek the state’s warm climate and lifestyle. Population growth fuels housing demand, pushing up both rental and purchase prices and creating strong demand for new housing supply.

Median dwelling prices

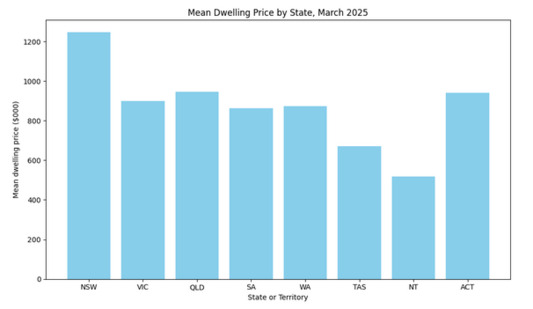

The Australian Bureau of Statistics (ABS) publishes quarterly statistics on the total value of the nation’s dwelling stock and the mean price of residential dwellings. In the March 2025 quarter the mean dwelling price across Australia reached $1,002,500, while Queensland’s mean dwelling price climbed to $944,700, overtaking the ACT to become the second highest in the country. New South Wales remained the most expensive at $1,245,900. Figure 1 illustrates the mean dwelling price by state.

The table below summarises the mean dwelling price for each state and territory as at March 2025.

| State/territory | Mean dwelling price (Mar 2025) |

| New South Wales (NSW) | $1,245,900 |

| Victoria (VIC) | $899,700 |

| Queensland (QLD) | $944,700 |

| South Australia (SA) | $861,900 |

| Western Australia (WA) | $874,200 |

| Tasmania (TAS) | $670,200 |

| Northern Territory (NT) | $517,700 |

| Australian Capital Territory (ACT) | $941,300 |

Housing supply and building approvals

Housing supply is heavily influenced by the number of new dwellings approved and completed. The ABS Building Approvals series tracks monthly and quarterly changes in the number of dwellings approved for construction. In the March 2025 release the ABS reported that total dwelling approvals across Australia fell 8.8 % to 15,220 units, while approvals for private sector houses fell 4.5 %. Queensland bucked the national trend for total dwellings: total dwelling approvals rose 5.8 % in the seasonally adjusted figures, even though approvals for private sector houses in the state fell 8 %. Queensland recorded 1,815 private sector house approvals and 3,116 total dwelling approvals in the month.

These statistics highlight that, although Queensland’s overall dwelling approvals increased, the state still faces a shortage of stand‑alone house approvals relative to the level of demand. Tight supply of existing detached homes has been a major factor pushing up house prices across the state. People choosing to build are therefore filling a supply gap and potentially gaining more choice and value compared with buying an established house in a heated market.

Buying an Existing Home

Buying an existing home is a familiar path for many. It involves selecting a property listed for sale, making an offer, securing finance and completing the legal transfer of ownership. While less complex than building from scratch, purchasing an established house carries its own set of advantages and disadvantages.

Advantages of buying

- Immediate occupancy. Once the purchase is settled, buyers can move in immediately without waiting months for construction. This is attractive for those needing a home quickly or who do not want the inconvenience of renting during a build.

- Established neighbourhoods. Older suburbs often boast mature trees, schools, cafes, public transport and community facilities that take decades to develop. Buying into an existing community can offer convenience and character not found in new estates.

- Historic or character features. Queenslanders love the charm of heritage homes—particularly classic “Queenslander” houses with wide verandas, high ceilings and timber details. Such features can be expensive or impossible to replicate in a new build.

- Predictable costs. The purchase price is known upfront. While there may be maintenance and renovation costs later, there is less risk of cost blowouts compared with the unpredictability of construction.

Disadvantages of buying

- Limited customisation. Buyers must accept the house’s existing layout and finishes unless they undertake renovations. Changing key features (for example, adding a bedroom or reconfiguring the kitchen) may require major structural work and council approval.

- Potential maintenance issues. Older homes may hide problems such as termite damage, wiring defects, outdated plumbing, asbestos or structural issues. Building and pest inspections are essential to identify these risks, but repairs and upgrades can be costly.

- Lower energy efficiency. Homes built under older standards typically have poorer insulation, less efficient windows and appliances and higher running costs. Upgrading to meet modern efficiency standards can be expensive.

- Competition. In high‑demand suburbs buyers often face auction bidding wars and limited stock, driving prices upward.

Costs associated with buying

- Purchase price. The most significant cost is the agreed sale price. Buyers usually need to provide a deposit (often 10 %) when exchanging contracts and pay the balance on settlement.

- Stamp (transfer) duty. Transfer duty is a state tax based on the purchase price. Concessions apply to first‑home buyers and off‑the‑plan purchases. From 1 May 2025, the Queensland Government removed stamp duty for first‑home buyers purchasing new homes or vacant land to build on. Eligible first‑home buyers can save around $9,096 on a median‑priced house‑and‑land package.

- Conveyancing and legal fees. Buyers should engage a solicitor or conveyancer to review contracts, conduct searches and settle the transaction. Fees typically range from $1,000 to $2,500, depending on complexity.

- Building and pest inspections. Pre‑purchase inspections reveal structural issues, safety hazards and pest infestations. They cost several hundred dollars but can save thousands in repairs.

- Lenders mortgage insurance (LMI). If the buyer’s deposit is less than 20 % of the purchase price, the lender may require LMI, which protects the lender if the borrower defaults.

- Insurance and ongoing costs. Home insurance, council rates, utilities and maintenance should be factored into the overall budget.

The buying process

- Research the market. Explore suburbs of interest, median prices, infrastructure and development plans. Consider lifestyle factors, proximity to work or schools, and future resale potential.

- Get finance pre‑approval. Approach lenders or mortgage brokers to determine borrowing capacity and secure pre‑approval. Pre‑approval provides confidence to make an offer and may strengthen bargaining power.

- Inspect properties. Attend open homes and private inspections, taking note of the layout, condition, aspect and neighbourhood. Ask the selling agent about recent comparable sales and reasons for selling.

- Due diligence. Commission building and pest inspections, check flood or bushfire overlays and review strata reports for units. Your solicitor will conduct title searches and examine the contract.

- Make an offer. Offers may be made via private treaty or at auction. Negotiate price, settlement period and conditions (such as finance or inspection clauses).

- Exchange contracts and pay deposit. Once the offer is accepted, both parties sign the contract. A deposit (typically 10 %) is paid and the cooling‑off period begins (except at auction).

- Settlement. On the agreed settlement date, the remaining funds are transferred, legal documents are lodged and the buyer receives the keys. Settlement periods usually range from 30 to 90 days.

Building a New Home

Building a home allows buyers to create a dwelling tailored to their lifestyle, design preferences and future plans. It involves purchasing land, engaging design professionals, obtaining approvals, selecting a builder and overseeing construction. Despite its complexity, building can offer significant rewards, especially when access to government incentives is factored in.

Advantages of building

The advantages of constructing a new home were succinctly summarised by South East Queensland builder Ausmar Homes. The company noted that building grants complete control over design and features, allowing buyers to choose the floor plan, number of bedrooms, bathrooms and kitchen size to create their dream home. New homes incorporate the latest technology and energy‑efficient features, offering modern amenities. They also come with warranties on appliances, fixtures and the structure itself, providing peace of mind. Finally, moving into a brand‑new home offers a “fresh start” with no hidden problems or outdated features.

Beyond these points, building offers the following benefits:

- Energy efficiency and sustainability. The National Construction Code 2022 (NCC 2022) requires new houses and town houses in Queensland to achieve a minimum 7‑star energy equivalence rating for the building envelope. The standards, implemented on 1 May 2024, also introduce a whole‑of‑home energy budget that accounts for appliances and on‑site renewable energy. Features such as northern orientation, optimized window placement, shading, roof and wall insulation, roof ventilation, light‑coloured roofs and ceiling fans can achieve the 7‑star rating. A new build allows home owners to integrate these features from the start, reducing energy bills and improving comfort.

- Lower maintenance costs. Everything is new, so major repairs should not be necessary for many years. Warranties cover structural issues and major appliances.

- Modern technology. New builds can incorporate smart home systems, energy‑efficient appliances, solar PV, battery storage, electric‑vehicle charging infrastructure and integrated security systems.

- Safety and resilience. Contemporary building codes incorporate improved fire safety, structural integrity and cyclone resilience. In Queensland, building codes address region‑specific risks like cyclones in the north.

- Stamp duty savings for first‑home buyers. From 1 May 2025, first‑home buyers in Queensland who enter a contract to purchase a new home or vacant land to build a home they will live in receive a full transfer duty concession. This policy makes building a new home more attractive compared with buying an established home above the exemption threshold.

- Eligibility for the First Home Owner Grant (FHOG). Buyers of new homes may be eligible for a $30,000 grant under the First Home Owner Grant scheme. The Queensland Government extended the boosted $30,000 grant until 30 June 2026. To qualify, buyers must sign an eligible contract between 20 November 2023 and 30 June 2026 and the total value of the home and land must be less than $750,000. The grant is available to those building or buying a new home, including owner builders whose foundations are laid within the eligibility window.

Disadvantages of building

- Longer timeframe. Constructing a home typically takes 6–12 months or longer, depending on the complexity of the design, availability of trades and materials, weather and council approval time frames. Owners must be prepared to continue renting or living elsewhere during the build.

- Up‑front and holding costs. Building requires upfront expenditure to buy land, pay design and approval fees and make progress payments during construction. Owners may need to pay rent and interest on a construction loan simultaneously.

- Complexity and decision fatigue. Selecting a block, designing the home, choosing materials and fixtures, coordinating approvals and managing variations can be overwhelming. Professional advice from architects, building consultants and independent building inspectors is crucial.

- Risk of cost overruns. Unexpected soil conditions, changes in materials prices, labour shortages or design variations can result in additional costs. A contingency budget is essential.

- Interim maintenance. During construction the owner must monitor progress, attend inspections and maintain the site to ensure conditions of the building contract are met.

Costs involved in building

When building a new home there are two major cost components—land and construction. Other fees include professional services, approvals, finance and connecting services.

Land. The price of vacant land varies widely depending on location, size, zoning and availability of infrastructure. In south‑east Queensland, premium blocks in established suburbs near the coast can be as expensive as established homes, while land in new estates or regional areas is more affordable. Buyers should check flood zones, bushfire overlays, soil classification and council restrictions when assessing land.

Construction cost. The cost per square metre depends on build quality (standard, custom or architectural), materials, site conditions, design complexity and labour costs. Industry estimates suggest that new homes in Brisbane typically cost between $2,800 and $4,950 per square metre for detached houses built by volume builders, with custom builds and architectural homes costing more. For a 200 m² family home this translates to $560,000–$990,000 for construction alone. Readers should obtain multiple quotes and consider including provisional sums and contingencies when budgeting.

Site preparation and external works. Clearing the block, levelling, retaining walls, slab or pier foundations, driveways, landscaping, fencing and connecting utilities can add tens of thousands of dollars to the budget.

Professional fees. Architects or building designers typically charge a percentage of construction cost (e.g., 6–12 %) or a fixed fee. Engineers (structural, hydraulic) are needed for site design and certification. Independent building inspectors can provide oversight at various stages.

Approvals and permits. Council approval fees, building certification and energy assessments must be budgeted. The NCC 2022 energy efficiency requirements may require specialised assessment to demonstrate compliance with the 7‑star standard.

Finance costs. Construction loans are usually interest‑only during the build. Lenders release funds in progress payments as stages of construction are completed. Because only part of the loan is drawn at the beginning, interest costs increase progressively. Budgeting for fluctuations in interest rates is important.

Insurance. Builders must hold QBCC home warranty insurance for work over $3,300, and owners should insure the structure and public liability once building commences.

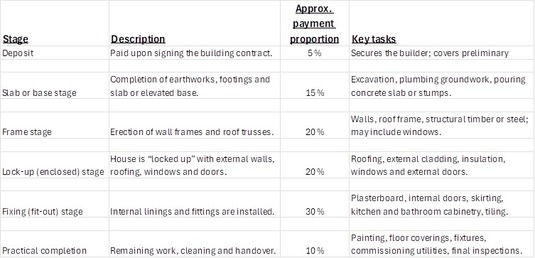

Construction process and stages

Although the specifics vary between builders, most new homes follow similar stages. A typical six‑stage payment schedule is outlined below. The percentages are approximate and may be adjusted by the contract or the builder:

At each stage the builder issues an invoice supported by evidence that the work has been completed. Owners should arrange independent inspections (for example by a building consultant) to ensure quality and compliance before paying.

Navigating building contracts

Building contracts in Queensland are governed by the Queensland Building and Construction Commission (QBCC) Act 1991. Common contract types include fixed‑price, cost‑plus and design‑and‑construct agreements. Key provisions to understand include:

- Scope of work. The contract should clearly define what is included and excluded, including provisional sums and prime cost items for fixtures and finishes. Ambiguity can lead to disputes.

- Progress payments. The contract sets out when payments are due and the proportion of the total contract price at each stage. The QBCC Act limits the maximum deposit (often 5 % for contracts over $20,000) and requires that progress payments reflect the value of work completed.

- Variations. Changes to materials or design after the contract is signed usually incur additional cost and time. Variation requests must be documented and approved.

- Time for completion. The builder should provide a practical completion date. Delays caused by the owner (for example, late selections) may entitle the builder to extensions of time.

- Defects liability period and warranties. After completion the builder remains responsible for rectifying defects for a specified period (typically 12 months). Structural warranties may extend for six years or more.

- Dispute resolution. The contract should outline procedures for dealing with disagreements. The QBCC provides mediation and adjudication services for building disputes.

Land and Location Considerations

Choosing the right location

Whether buying or building, location is one of the most critical determinants of long‑term satisfaction and capital growth. Consider the following factors when selecting a suburb or region:

- Proximity to employment. Commuting time affects daily life. Locations near employment centres, public transport hubs and major roads command higher prices but may reduce transport costs.

- Schools and childcare. Families prioritise catchment areas for high‑performing public schools and availability of childcare services. Many suburbs publish school enrolment boundaries, so verify that your desired property falls within them.

- Amenities and lifestyle. Parks, beaches, shopping centres, medical facilities, sporting clubs and entertainment venues contribute to quality of life. The Sunshine Coast and Gold Coast provide beachside living, while Brisbane offers urban conveniences.

- Future infrastructure. Research planned transport upgrades, new schools, hospitals and industrial projects. Areas slated for infrastructure investment often experience capital growth.

- Environmental risks. Check local council planning overlays for flood, bushfire, landslip or coastal erosion hazards. Properties in high‑risk areas may require special construction standards or be uninsurable.

- Zoning and development. Council planning schemes identify zones (residential, mixed use, rural) and development densities. Understand whether the area is earmarked for infill development, apartments or industrial use, as this will affect neighbourhood character.

Site considerations when building

The characteristics of your building site influence design, cost and construction difficulty:

- Topography. Sloping blocks may require split‑level designs, retaining walls and additional engineering. Flat sites are generally cheaper to build on.

- Soil type. Highly reactive clay or rocky soils need deeper footings or specific engineering solutions, increasing costs. A geotechnical (soil) report will inform foundation design.

- Orientation. North‑facing living areas maximise natural light and reduce heating costs. Correct orientation is crucial for achieving the 7‑star energy rating.

- Access. Narrow or battle‑axe blocks can limit access for construction vehicles and increase build complexity.

- Easements and services. Ensure there is legal access to water, sewerage, electricity and telecommunications. Easements may restrict where you can build.

- Covenants and design guidelines. Many new estates impose design guidelines dictating façade styles, roof colours, fencing and landscaping. Understand these rules before choosing a block.

Environmental and Sustainability Considerations

Regulatory standards

Queensland has adopted the National Construction Code 2022, which raises the minimum energy efficiency requirements for new dwellings. From 1 May 2024, new houses and town houses in Queensland must achieve a 7‑star energy equivalence rating for the building shell and comply with a whole‑of‑home energy budget. This regulation is implemented through the Queensland Development Code 4.1 – Sustainable Buildings. The mandatory 7‑star rating encourages passive design (orientation, ventilation, shading) and insulation, and it considers major appliances and on‑site renewable energy such as solar photovoltaic systems.

Design features for energy efficiency

To achieve high energy ratings and reduce running costs, consider incorporating the following design features:

- Orientation and layout. Position living areas to the north, bedrooms to the east and west and minimise openings on the west. This maximises winter sun and minimises summer heat gain. Good cross‑ventilation helps cool the home naturally.

- Shading and glazing. Use eaves, awnings, pergolas, external blinds and vegetation to shade windows. Select low‑emissivity or tinted glass to reduce heat transfer, especially on western elevations.

- Insulation. Install bulk insulation in the roof and walls, reflective foil under roofing and wall membranes. Ventilating the roof space via vents prevents heat build‑up.

- Roof colour. Choose light‑coloured roofing and external walls to reflect heat.

- Ceiling fans and natural ventilation. Ceiling fans in living areas and bedrooms promote air circulation and reduce reliance on air‑conditioning.

- Outdoor living areas. Incorporate decks or verandas with good orientation; these can count towards achieving the 7‑star rating.

- Solar PV and battery storage. Installing solar panels offsets household electricity consumption, and batteries can store excess energy for evening use. Many builders offer packages including solar PV.

- Water efficiency. Harvest rainwater in tanks for garden or toilet use and install water‑efficient fixtures. Queensland has periods of drought, making efficient water use essential.

- Sustainable materials. Use low‑embodied‑energy materials (recycled timber, locally sourced materials), low‑VOC paints and sustainably sourced timber. Choose durable cladding that requires minimal maintenance.

Environmental benefits of new homes

New homes can significantly reduce energy consumption compared with older housing stock. Improved insulation, air‑tightness and efficient appliances lower heating and cooling demands, resulting in reduced greenhouse‑gas emissions. As renewable energy adoption grows and the grid becomes greener, new homes designed for energy efficiency will have an even smaller carbon footprint. Over the life of the home, the cost savings on energy bills can offset a portion of the initial investment in sustainable features.

Legal and Financial Frameworks

Government incentives and grants

First Home Owner Grant. The Queensland Revenue Office offers a grant to first‑home buyers who build or purchase a new home. Contracts signed between 20 November 2023 and 30 June 2026 (inclusive) qualify for a $30,000 grant. The total value of the home and land must be less than $750,000. Owner builders who lay foundations during the same period are also eligible. Read more: https://qro.qld.gov.au/property-concessions-grants/first-home-grant/

Stamp (transfer) duty concession. From 1 May 2025, first‑home buyers who purchase a new home or vacant land to build a home to live in are exempt from transfer duty. This policy aims to reduce transaction costs and support housing affordability. It is distinct from the First Home Owner Grant and can be used in conjunction with it.

Home guarantee schemes. National initiatives administered by Housing Australia, such as the First Home Guarantee and Regional First Home Buyer Guarantee, allow eligible buyers to purchase a home with deposits as low as 5 % without paying lenders mortgage insurance. These schemes operate alongside state grants but have separate eligibility criteria.

Financing the build

Construction loans. Construction loans differ from standard mortgages. The lender approves the total loan amount based on the land value and construction contract, but funds are drawn down in stages. Borrowers pay interest only on the amount drawn at each stage. Lenders send a valuer to verify progress before releasing funds. Some lenders charge a slightly higher interest rate for construction loans or may require a larger deposit.

Cash reserves and contingencies. Building projects often experience variations and unexpected costs. A contingency of 10 % of the contract value is recommended. Owners should also have cash reserves to cover rent or mortgage payments during construction.

Bridging finance. Home owners selling an existing property to fund the construction of a new home may use bridging finance to cover the period between purchase and sale. Bridging loans can be more expensive and carry greater risk if the original property takes longer to sell.

Insurance and warranties

- Builder’s insurance. Registered builders in Queensland must provide home warranty insurance through the QBCC for work over $3,300. This covers defects and incomplete work in the event the builder dies, disappears or becomes insolvent.

- Owner’s building insurance. Once the slab is poured, owners should take out construction insurance covering theft, vandalism, fire and public liability. Lenders typically require proof of insurance before releasing funds.

- Defects liability period. After handover, the builder must rectify defects identified within the defect liability period (usually 12 months). Structural warranties may extend for six years. Keep records of all correspondence and inspections.

Risk Management and Hidden Costs

Risks when buying

- Structural defects and maintenance. A pre‑purchase inspection may not uncover every issue. Budget for unexpected repairs, especially in older properties.

- Market volatility. Buying at the top of the market can expose purchasers to short‑term price declines. Consider your time horizon; property is generally a long‑term investment.

- Hidden costs. Renovations to bring an older property up to modern standards—electrical rewiring, plumbing, insulation, asbestos removal—can be significant.

- Pest and environmental risks. Termites, rising damp or contamination can pose risks.

Risks when building

- Cost overruns. Changes in materials costs, design variations or unexpected site conditions can drive up costs. A fixed‑price contract with defined allowances can limit risk but may restrict choice.

- Delays. Weather, supply chain disruptions, labour shortages and slow council approvals can delay completion. Delays increase holding costs and may impact financing.

- Builder insolvency. If a builder collapses mid‑project, owners may have to find another builder and incur additional costs. Ensure the builder is licensed, financially stable and has appropriate insurance.

- Quality issues. Poor workmanship can result in costly repairs later. Engage independent inspectors at key stages and hold the builder to contractual obligations.

- Regulatory changes. Changes to building codes or zoning regulations can require design modifications, increasing costs or causing delays.

Mitigation strategies

- Conduct thorough due diligence. For buyers, invest in quality inspections and legal advice. For builders, commission soil tests, site surveys and independent cost estimates.

- Choose reputable professionals. Research builders’ licences, references and portfolios. Ask about experience with similar projects and check online reviews.

- Budget contingencies. Allow for contingencies in both building and buying budgets. Factor in interest rate increases and unexpected repairs.

- Document everything. Maintain written records of communications, variations, invoices and inspections.

- Stay involved. Attend site inspections, track progress and communicate regularly with your builder or agent.

Comparative Analysis: Buy vs Build

Cost comparison

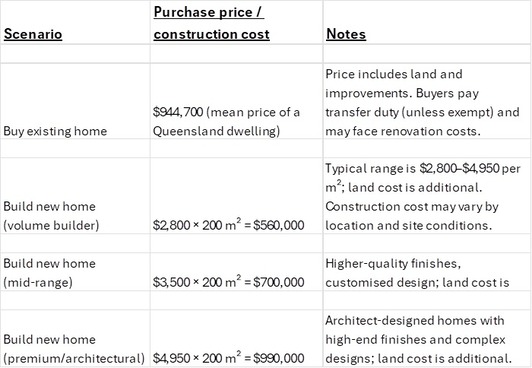

The cost of buying an established home versus building a new one depends on many variables, including location, size, level of finish and market conditions. Nevertheless, a simplified comparison helps illustrate typical differences. Using the ABS data for mean dwelling prices (March 2025) and typical building cost ranges, the following table compares a 200 m² detached home in Queensland.

The above figures suggest that building a new home can be cheaper or more expensive than buying an established home depending on land cost and the quality of the build. Buyers must also account for the cost of renting during construction, whereas buyers of existing homes can move in immediately. On the other hand, new homes may qualify for grants and stamp duty exemptions that reduce the effective cost by tens of thousands of dollars.

Timeframes

- Buying. Once finance is approved, a purchase can settle in as little as 30 days (longer if the seller requests a longer settlement). Renovations or repairs may extend the move‑in timeframe.

- Building. Allow 2–4 months for design, approvals and obtaining finance, followed by 6–12 months for construction. Weather, material shortages and changes may extend the timeline. Early planning and prompt selections can minimise delays.

Flexibility and customisation

Building offers unmatched flexibility to design a home that suits your needs now and in the future. You control layout, finishes, energy features and accessibility (for example, universal design). Buying restricts choices to the existing layout unless you undertake significant renovations.

Risk profile

Key trade‑offs

When deciding whether to buy or build, consider the following trade‑offs:

- Capital growth versus customisation. Established suburbs often deliver stronger capital growth due to scarcity of land and entrenched amenity. New estates or regional areas may have slower growth but allow customisation and energy‑efficient homes.

- Cashflow. Building requires paying for land and construction before you can live in the home. Buying may have higher upfront costs but avoids renting and construction loan interest.

- Lifestyle. Are you looking for a particular character or community vibe that only an established suburb offers? Or do you prefer to shape your own environment? Consider proximity to schools, work and lifestyle amenities.

- Risk tolerance. Building involves managing more variables. If you are risk‑averse or time‑poor, buying may be less stressful. If you enjoy project management and want control over outcomes, building might suit you.

Decision‑Making Framework

Making a decision requires balancing quantitative factors (costs, time, incentives) with personal priorities (lifestyle, design preferences, tolerance for risk). The following framework can assist:

- Establish your budget. Consider savings, borrowing capacity and affordability over the long term. Include contingency funds for variations or repairs.

- Define your must‑haves and nice‑to‑haves. List the features that are non‑negotiable (e.g., number of bedrooms, accessibility) and those you can compromise on. Determine whether these needs can be met more easily by building or buying.

- Assess location options. Compare established suburbs and new developments. Consider proximity to work, schools and transport. Evaluate land availability and pricing.

- Research market conditions. Evaluate current and projected property prices, interest rates and construction costs. Understand how market cycles could impact your decision.

- Investigate government incentives. Determine eligibility for the FHOG, stamp duty concessions and guarantee schemes. Calculate the net benefit of these incentives.

- Evaluate timeline. Consider how soon you need to move and whether you can manage renting during construction. Account for potential delays.

- Consult professionals. Speak with mortgage brokers, builders, architects, real‑estate agents and financial advisers. Independent advice can clarify costings and risks.

- Make a comparative analysis. Use tables or spreadsheets to model different scenarios, accounting for purchase price, build costs, incentives, rental expenses during construction and potential renovation costs for older homes.

- Review your risk tolerance. Consider how you would respond if costs increase or the market turns. Building requires a higher risk appetite and more hands‑on involvement.

Profile: Ward Builders – Sunshine Coast

Ward Builders is a family‑owned building company based in Coolum Beach on the Sunshine Coast. Established in 2005, the company specialises in custom homes, extensions, renovations and apartment renovations. According to its website, Ward Builders is committed to “bringing ideas to life with uncompromised quality.” They emphasise a client‑centric approach, transparent costs, clear project roadmaps and quality craftsmanship so clients feel “empowered and relaxed from the very beginning.”. Their collaborative approach ensures clients are involved throughout the process, with all costs and timelines communicated clearly.

The company’s website highlights its 20 years of experience and modern systems, describing the team as “exceptional humans” building unique homes and transformations. Ward Builders showcases several projects on its site—ranging from custom builds to granny‑flat extensions and penthouse renovations. Testimonials from designers and repeat clients praise the builder’s quoting accuracy, communication, craftsmanship and ability to execute high‑end designs. Customers note that Ward Builders’ attention to detail and collaborative approach set them apart.

Ward Builders offers the following services:

- Custom homes. Bespoke homes designed to suit client specifications and budgets. Read more: https://wardbuilders.com.au/building-services/custom-homes/

- Extensions. Additions to existing homes, such as extra bedrooms, living areas or granny flats. Read more: https://wardbuilders.com.au/building-services/home-extensions/

- Renovations. Transformations of kitchens, bathrooms, living spaces and entire homes. Read more: https://wardbuilders.com.au/building-services/renovations/

- Apartment renovations. Makeovers for apartments and penthouses, including structural modifications and high‑end finishes. Read more: https://wardbuilders.com.au/building-services/apartment-renovations-2/

Ward Builders is licenced by the QBCC (licence number 1272680) and serves the Sunshine Coast region, including Noosa Heads, Maroochydore and surrounding suburbs.

Other local builders

Homes by CMA

Homes by CMA deliver an excellent blend of value and flexibility for Sunshine Coast homebuyers, offering comprehensive home-and-land packages and a strong emphasis on transparent, upfront pricing—including colour, electrical and interior selections before contract signing. Their design studio and display homes (e.g. Aura at Caloundra) make it easy to visualise your dream home, and their reputation for personalised service and interior guidance provides great peace of mind. https://www.homesbycma.com.au/home-land-packages-sunshine-coast/

Nest Homes (Nest Homes / Nest Bespoke)

Nest Homes is a custom home builder known for high‑quality craftsmanship and tailored service on the Sunshine Coast. They focus on delivering client-first outcomes with strong communication throughout the process, making your build feel not only bespoke but genuinely collaborative. https://www.buildnest.com.au/

Roonsleigh Constructions

Roonsleigh Constructions specialise in turning houses into homes with an emphasis on quality and attentive service—going the extra mile throughout the build to ensure each project is welcoming and personally tailored. Their strong reputation is further supported by excellent customer reviews. https://www.roonsleigh.com.au/

Brighton Homes

Brighton Homes is one of the Sunshine Coast’s most respected builders, boasting over 30 years’ experience and recognised with the 2022 HIA Professional Major Builder Award. They offer tailored home designs—from acreage to narrow‑lot homes—with inclusive packages, knock‑down rebuild options, and multiple display homes across the region. The combination of craftsmanship, community consciousness and flexibility makes them a standout choice. https://www.brightonhomes.net.au/building-guide/where-we-build/sunshine-coast

Pacific Blue Custom Home Builders

Pacific Blue has built a strong reputation across the Sunshine Coast as luxury custom home providers since 2000. With over 400 custom homes completed, they focus on a seamless, relationship‑driven process—from initial design through construction—with long‑term local craftsmen embedded in their team. Their transparent, stress‑free approach ensures the journey feels just as personal as the final product. https://pacific-blue.com.au/

References:

https://wardbuilders.com.au/

https://www.abs.gov.au/statistics/economy/price-indexes-and-inflation/total-value-dwellings/mar-quarter-2025

https://aplacetocallhome.initiatives.qld.gov.au/stamp-duty-concession

https://www.housing.qld.gov.au/initiatives/modern-homes/residential-energy-efficiency-standards

https://qro.qld.gov.au/property-concessions-grants/first-home-grant/eligibility/

https://ausmarhomes.com.au.